Your retirement planning hinges on a complete understanding of Social Security benefits, yet hidden rules and complex calculations often blindside even meticulous savers. Mastering these obscure regulations prevents you from leaving thousands of dollars on the table and secures your retiree finances against unexpected shortfalls. While many people view this federal program as a straightforward monthly check based on past earnings, the system features intricate claiming strategies, taxation thresholds, and spousal nuances that dramatically alter your lifetime payout. You must navigate these structural complexities to maximize your ultimate return on decades of payroll contributions. Grasping these essential Social Security facts equips you to optimize your claiming timeline and fortify your financial independence during your post-career years.

Fast Facts

Although you pay into the system using after-tax dollars during your working years, the federal government subjects up to 85 percent of your Social Security benefits to income taxes if your combined provisional income exceeds specific IRS thresholds. You must carefully manage your retirement withdrawals from traditional tax-deferred accounts to keep your provisional income low; failure to control these distributions forces you to surrender a massive portion of your earned benefits to excessive federal taxation.

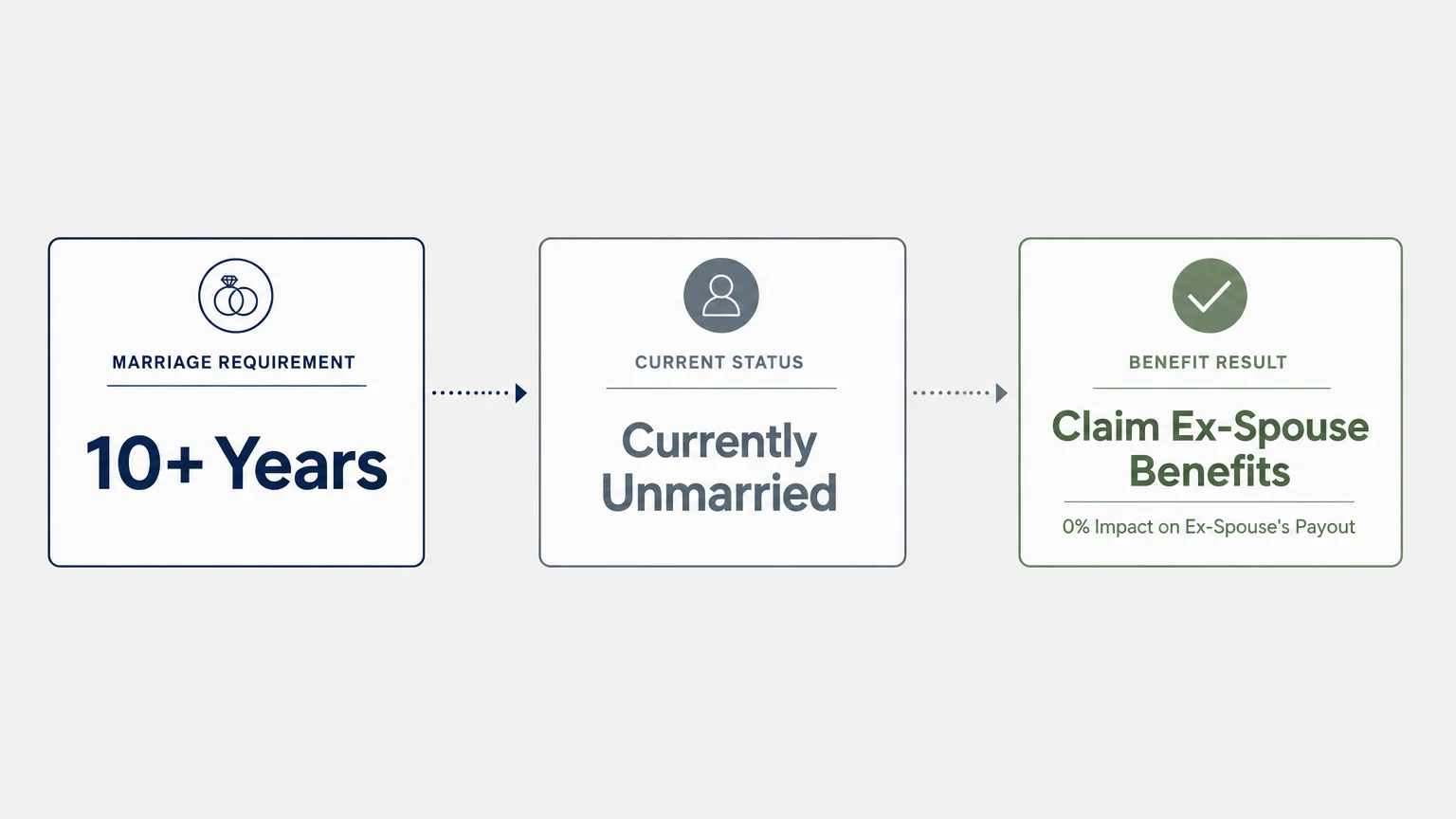

You hold the right to claim benefits based on an ex-spouse’s work record if your marriage lasted at least ten consecutive years and you currently remain unmarried. Accessing this divorced spouse benefit does not reduce the payout your ex-spouse or their current partner receives; it simply leverages their higher earning history to legally boost your personal retiree finances. Taking advantage of this completely independent claiming mechanism secures a larger financial baseline without requiring any communication or coordination with your former partner.

Claiming your monthly check before reaching full retirement age while continuing to work full-time subjects you to the retirement earnings test, which temporarily withholds one dollar in benefits for every two dollars you earn above an established annual limit. Fortunately, the administration does not permanently confiscate this money; they automatically recalculate your benefit formula once you reach full retirement age to slowly return the withheld funds through higher monthly payments over the remainder of your life.

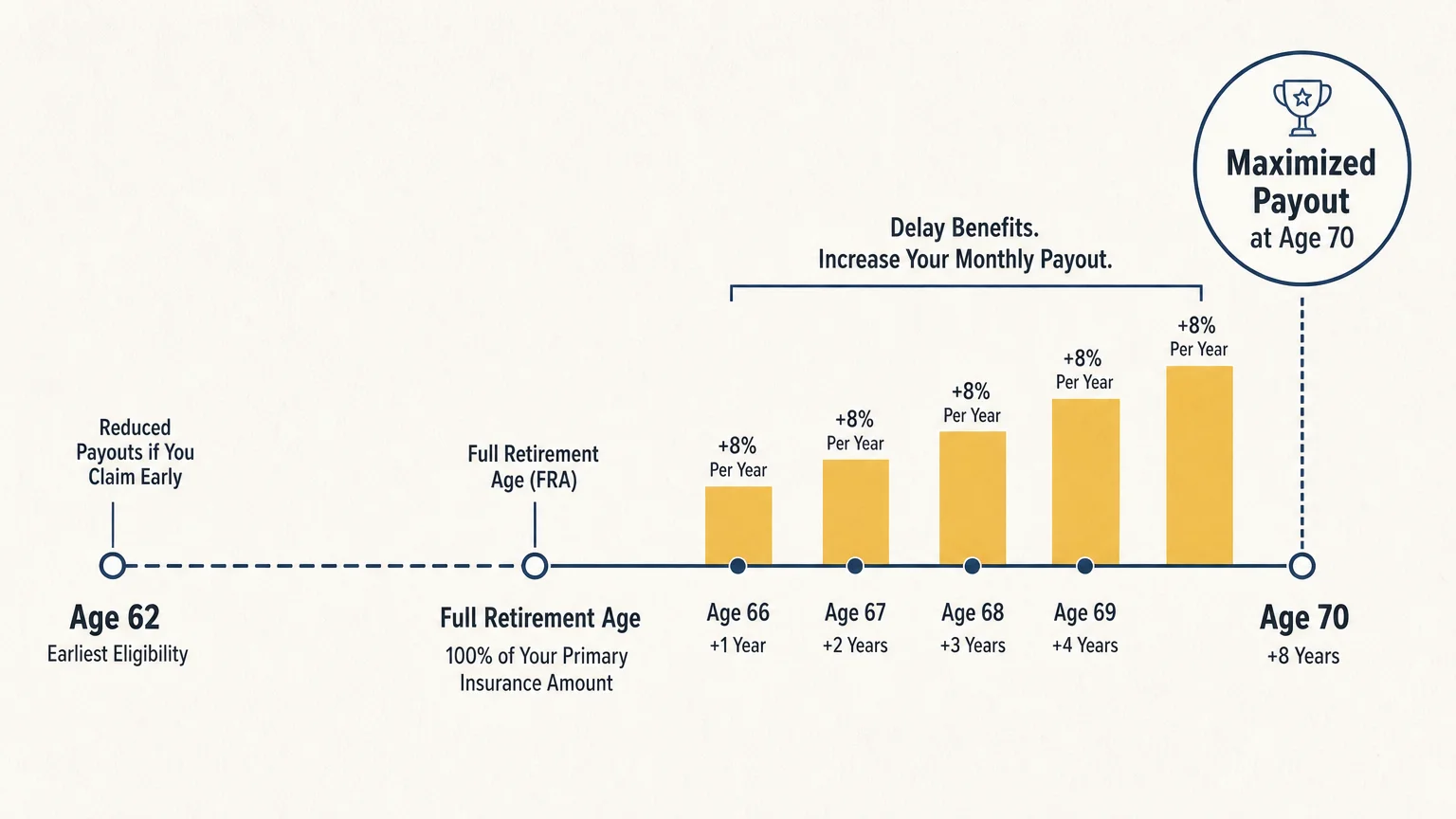

Every single year you delay claiming your benefits beyond your designated full retirement age guarantees an eight percent increase in your monthly payout up until you reach age 70. This delayed retirement credit serves as one of the most powerful tools in retirement planning—offering a guaranteed, inflation-adjusted, risk-free return that absolutely no private market investment portfolio can reliably replicate over a similar timeframe.

Your actual bank deposit often falls surprisingly short of your official benefit amount because the government automatically deducts Medicare Part B premiums directly from your Social Security checks before issuing payment. Furthermore, realizing significant capital gains or executing massive Roth conversions can trigger the Income-Related Monthly Adjustment Amount surcharge; this penalty drastically increases your Medicare premiums and effectively shrinks your net Social Security payout for the entire calendar year.

If you initiate your retirement benefits while actively caring for dependent children under age 18—or under age 19 if they still attend high school on a full-time basis—they individually qualify to receive up to half of your full retirement benefit amount. This family maximum provision provides crucial supplementary income for older parents and grand-families navigating late-stage childrearing, though an overarching cap prevents the combined household payout from exceeding roughly 150 to 180 percent of your foundational base benefit.

Surviving spouses possess the unique, incredibly valuable flexibility to actively coordinate their claiming sequence by drawing a survivor benefit first while allowing their personal retirement benefit to grow untouched, or vice versa. This strategic sequencing requires meticulous calculation but ultimately maximizes your lifetime household payout by ensuring you capture the highest possible delayed retirement credits on whichever earning record yields the largest permanent monthly check.

Annual Cost of Living Adjustments do not merely provide a temporary, isolated inflation hedge; they permanently compound the foundational base figure used to calculate all your future benefit increases. Because these percentage hikes apply directly to your primary insurance amount regardless of your specific claiming age, delaying your application until age 70 mathematically amplifies the absolute dollar value of every subsequent cost of living raise you receive throughout your lifespan.

The poorly understood Windfall Elimination Provision permanently and severely reduces your Social Security payouts if you also collect a pension from a job that did not withhold Social Security payroll taxes, such as specific teaching, police, or state government positions. You must incorporate this aggressive reduction into your retirement planning early, as the regulatory formula can instantly diminish your expected monthly check by more than five hundred dollars and thoroughly shatter your long-term income projections.

Beyond standard federal levies, a minority of specific states currently impose their own localized income taxes on Social Security benefits, utilizing entirely different income thresholds, age brackets, and exemption rules than the federal government. Relocating your primary residence to a tax-friendly jurisdiction can instantly and dramatically improve your retiree finances, though you must comprehensively weigh these specific tax savings against the broader cost of living, healthcare expenses, and property tax rates in your targeted destination state.

Context and Background

The federal government established the Social Security program in 1935 to provide a vital financial safety net for older Americans during the Great Depression. Since its inception, profound demographic shifts and massive legislative overhauls have drastically transformed how you must interact with the system today. Originally, the program supported a relatively small population of short-lived retirees using the payroll contributions from a massive, booming workforce. Today, increasing life expectancies and rapidly declining birth rates place unprecedented mathematical pressure on the system, completely altering the underlying realities of your retirement planning. The worker-to-beneficiary ratio plummeted from over sixteen contributing workers per retiree in 1950 to fewer than three workers per retiree today. You must factor this structural demographic shift into your long-term expectations and savings strategies.

To sustain the program through these unavoidable demographic changes, lawmakers enacted highly significant reforms in 1983. These comprehensive amendments gradually increased the full retirement age from 65 to 67 and introduced the taxation of benefits for the very first time. Understanding this historical pivot helps you recognize exactly why your expected payout timeline looks vastly different than the one your grandparents experienced. The federal government designed these structural changes to temporarily stabilize the Old-Age and Survivors Insurance Trust Fund, which holds the surplus payroll taxes collected over the past few decades. You should closely monitor the annual trustees’ report, as the trust fund reserves currently project complete depletion in the mid-2030s. If Congress fails to act before this critical depletion date, the system will rely solely on ongoing tax revenues, which would only cover roughly 80 percent of scheduled payouts.

Beyond sweeping demographics and federal legislation, the internal mathematical mechanics of benefit calculation precisely dictate your eventual payout. The Social Security Administration determines your primary insurance amount by indexing your lifetime earnings to account for historical wage growth and selecting your 35 highest-earning years. If you work fewer than 35 years in covered employment, the administration forcefully inserts zeros into your calculation, which severely drags down your overall average and permanently shrinks your monthly check. You can proactively replace these zero-income years by working a few additional years at the tail end of your career, even in a part-time capacity, to mathematically optimize your baseline benefit.

You can leverage this deep historical context to make pragmatic, emotionless decisions about your retiree finances. Recognizing the actual legislative mechanics behind the trust fund empowers you to safely ignore sensationalist media headlines claiming the program will go completely bankrupt and disappear. Instead, you can focus on actionable retirement tips, such as building robust supplemental income streams to heavily insulate yourself from potential future benefit reductions. Diversifying your retirement portfolio through individual retirement accounts, workplace 401(k) plans, and health savings accounts ensures you do not depend entirely on a federal system subject to congressional whims. By treating Social Security as a foundational insurance policy against outliving your assets rather than your sole wealth-building tool, you construct a resilient financial fortress capable of weathering both legislative adjustments and severe economic volatility.

Interesting Connections

Your Social Security benefits function remarkably like an inflation-adjusted single premium immediate annuity, creating a fascinating connection between federal policy and private insurance principles. When you intentionally delay your claim, you essentially purchase additional longevity insurance from the government that powerfully protects you against the devastating risk of outliving your money. Private insurance companies charge exorbitant upfront premiums for commercial policies offering guaranteed, inflation-linked lifetime payouts, yet the federal government provides this exact financial mechanism simply through delayed retirement credits. You maximize the immense value of this built-in public annuity by leaning heavily on your private investments during your early sixties, allowing your federal benefit to compound untouched until it reaches its maximum possible threshold.

Another compelling intersection exists between your chosen Social Security strategy and your household life insurance needs. Married couples must meticulously coordinate their claiming timelines to protect the surviving spouse, as the death of one partner immediately eliminates the smaller of the two household Social Security checks. By having the higher-earning spouse aggressively delay their claim until age 70, you definitively guarantee the surviving spouse inherits the largest possible ongoing monthly payment. This strategic delay often radically reduces the necessity for purchasing expensive permanent life insurance policies late in retirement. You can intelligently reallocate the exact money you would have spent on insurance premiums into income-generating assets, effectively utilizing the federal survivor benefit rules to mathematically optimize your broader portfolio.

On a macroeconomic level, the widespread distribution of Social Security funds acts as a crucial, invisible economic stabilizer for local communities across the entire country. Retirees consistently inject their monthly federal checks directly into local grocery stores, healthcare providers, regional retail centers, and local service sectors. This steady, reliable flow of capital sustains regional economies during severe economic downturns when consumer spending among the working-age population typically contracts. Recognizing this powerful macroeconomic connection highlights exactly why major proposed reductions in federal benefits would trigger widespread secondary effects, damaging local job markets and drastically reducing state and local tax revenues nationwide.

Finally, you must constantly connect your claiming strategy to the broader federal tax code to successfully preserve your retiree finances. Because the IRS strictly calculates your benefit taxation based on your combined provisional income, every single dollar you withdraw from a traditional, tax-deferred retirement account potentially exposes another 85 cents of your Social Security benefit to federal income tax. You can permanently disrupt this devastating tax torpedo by strategically utilizing Roth accounts throughout your late career and early retirement. Qualified distributions from Roth accounts absolutely do not count toward your provisional income, allowing you to draw substantial tax-free cash while artificially keeping your official IRS income low enough to legally protect your Social Security benefits from excessive taxation. Navigating this complex intersection of tax law and federal benefits defines sophisticated retirement planning.

Frequently Asked Questions

How does my continuing to work impact my benefits after I reach full retirement age?

Once you reach your precise full retirement age, the restrictive retirement earnings test disappears entirely. You can earn an unlimited amount of money from wages, corporate salary, or active self-employment without triggering any temporary reductions in your monthly Social Security check. Furthermore, your continued payroll tax contributions can actually increase your future payouts. The administration reviews your ongoing earnings record annually; if your current salary ranks among your 35 highest-earning years, they will automatically recalculate your primary insurance amount and issue a larger monthly check to perfectly reflect your updated, higher earning history.

Can I suspend my benefits if I change my mind after claiming?

You possess a strict, one-time opportunity to completely undo your claiming decision if you actively file a formal withdrawal of application within 12 months of first receiving your benefits. To properly execute this withdrawal, you must repay every single dollar you and your family received based on your application, including withheld federal taxes and deducted Medicare premiums. If you miss this tight 12-month window but have reached your full retirement age, you can voluntarily choose to suspend your benefits. Suspending your ongoing payments allows you to earn delayed retirement credits—boosting your future payout by eight percent annually until age 70—without requiring you to repay the funds you already collected.

Will my Social Security benefits cover my long-term care expenses?

You should absolutely not rely on Social Security to fund any significant long-term care requirements. The average monthly benefit barely covers basic civilian living expenses and falls drastically short of the exorbitant, rapidly inflating costs associated with nursing homes, memory care assisted living facilities, or continuous in-home medical care. You must implement separate, highly focused retirement tips to adequately address these healthcare risks, such as purchasing dedicated long-term care insurance, funding a health savings account, or earmarking a specific portion of your investment portfolio to absorb catastrophic medical costs that Medicare and Social Security explicitly ignore.

How do international relocations affect my ability to collect federal retirement benefits?

You can generally receive your full Social Security payments while living comfortably outside the United States, provided you reside in a country that maintains favorable banking and diplomatic security agreements with the federal government. The administration seamlessly deposits your funds electronically into international or domestic bank accounts. However, Medicare absolutely does not provide any medical coverage overseas. If you abandon your active Medicare Part B enrollment while living abroad and later decide to return to the United States, you will face severe, permanent late-enrollment penalties. You must carefully weigh the high cost of maintaining unused domestic health coverage against the lifestyle savings of international expatriation.

What protections shield my Social Security payments from aggressive debt collectors?

Federal law heavily fortifies your Social Security benefits against aggressive garnishment by private creditors, credit card companies, and private medical debt collectors. Even if you declare total personal bankruptcy, private creditors cannot legally seize your federal retirement income to satisfy outstanding unsecured personal debts. However, these robust protections completely vanish if you owe money directly to the government. The federal government can directly garnish your monthly check to forcibly recover unpaid income taxes, defaulted federal student loans, or delinquent child support and court-ordered alimony payments. You must properly segregate your Social Security deposits into a dedicated, unmixed bank account to clearly identify these protected funds if private debt collectors ever attempt to unlawfully freeze your assets.