The landscape of life after work shifts dramatically every year, forcing millions to rethink their financial futures. Americans now estimate they need $1.46 million to retire comfortably, yet more than half of households have zero dedicated retirement savings. The gap between expectation and reality creates immediate challenges, pushing many older adults back into the labor force while escalating healthcare expenses drain existing nest eggs. Understanding the current data surrounding senior living and wealth accumulation provides clarity for your own long-term strategy. By examining the latest benchmarks on median balances, medical costs, and changing timelines, you can pivot your approach and secure a sustainable income stream long before you hand in your final resignation.

Fast Facts

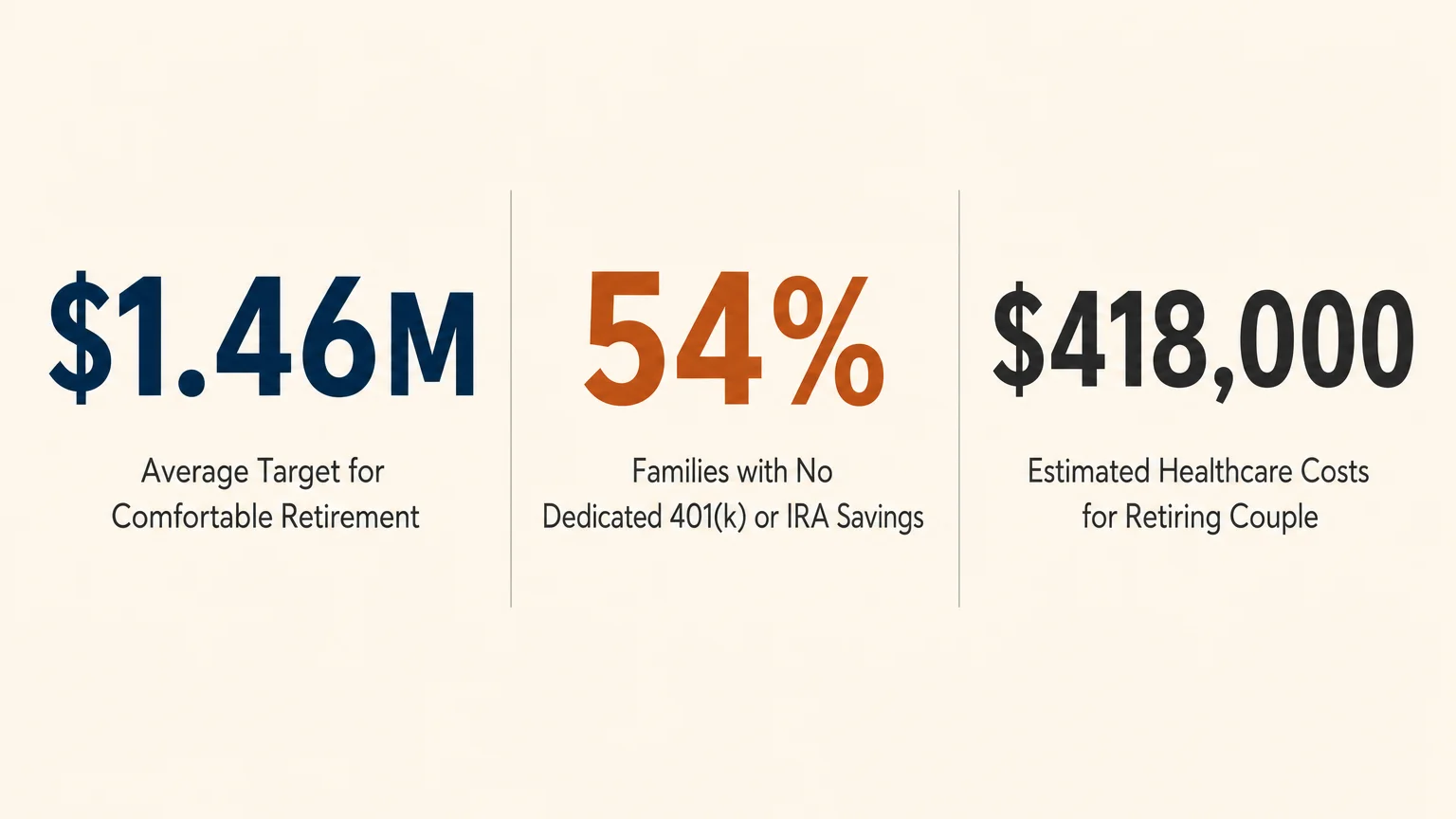

Americans now target an astonishing $1.46 million for a comfortable exit from the workforce. A recent Northwestern Mutual study reveals this figure jumped by $200,000 in a single year, highlighting how aggressive inflation permanently alters personal financial planning.

Despite ambitious wealth targets, over half of American households possess absolutely no dedicated retirement savings. The Federal Reserve indicates that 54% of families lack funds in 401(k)s or IRAs, leaving them entirely dependent on standard government benefits and whatever liquid assets they hold in standard bank accounts.

Medical expenses remain a colossal and expanding burden; a healthy 65-year-old couple retiring in 2026 needs an estimated $418,000 just to cover healthcare costs. According to the Milliman Retiree Health Cost Index, this figure accounts for Medicare premiums and out-of-pocket costs, emphasizing the critical need for specialized health savings strategies.

The timeline for stepping down is rarely entirely your own, as 46% of retirees leave the workforce earlier than they originally planned. Data from the Employee Benefit Research Institute notes that sudden health issues, corporate restructuring, and unexpected caregiving demands frequently force these premature exits, cutting short crucial wealth accumulation years.

The concept of permanent leisure is rapidly fading; nearly 1 in 8 seniors plan to return to work or already have reentered the labor force. Recent survey data shows this “unretirement” trend is largely driven by financial anxiety, proving that modern retirement operates more as a fluid transition rather than a hard stop.

Financial necessity drastically outweighs the desire for mental or social engagement among those returning to the labor market. Approximately 48% of unretirees go back to work simply because they need the money to cover basic expenses, whereas only 14% do so merely to stay active.

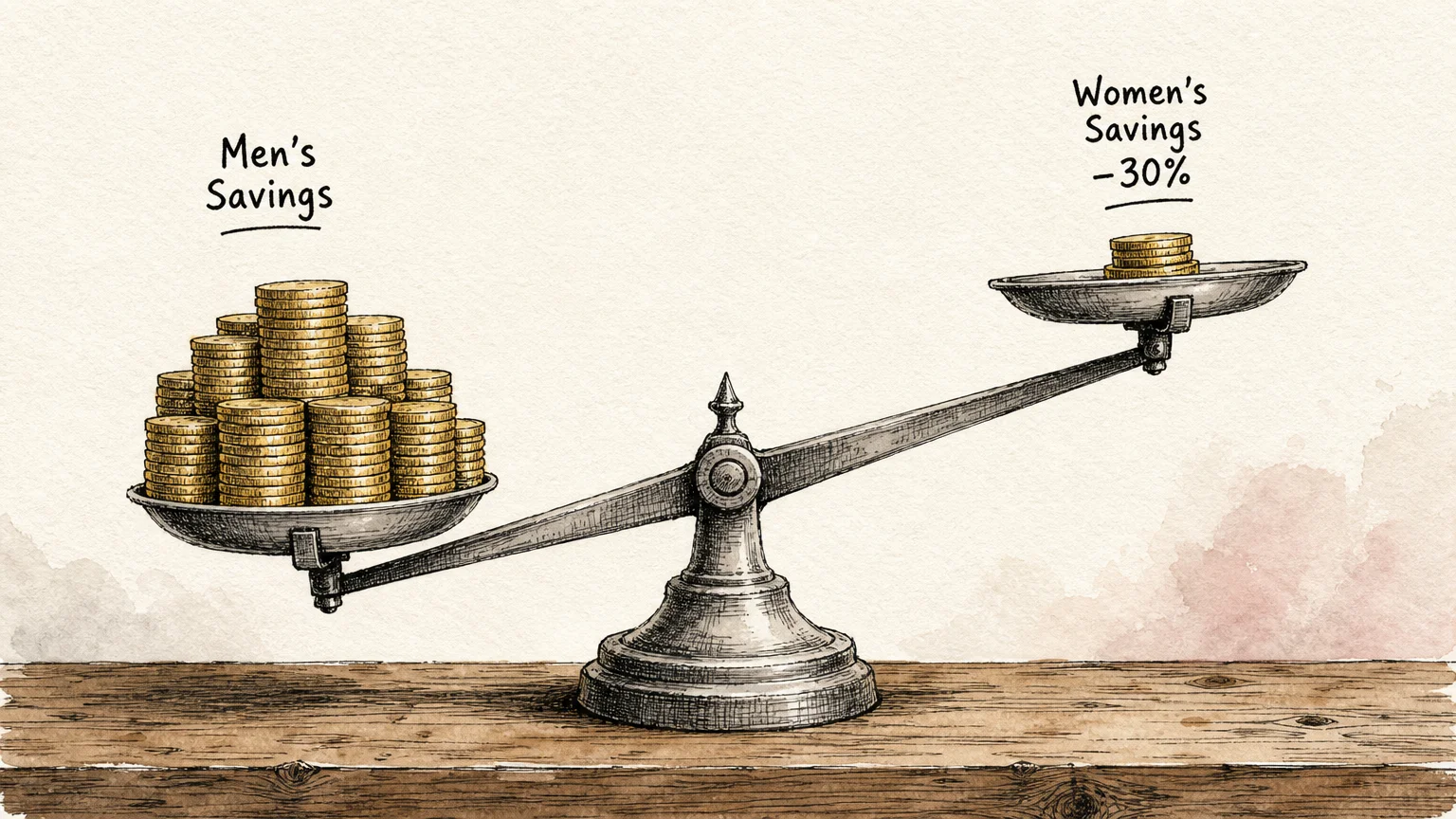

Women face a severe disadvantage in wealth accumulation, holding median retirement savings that are roughly 30% lower than men. Interrupted careers for caregiving responsibilities, persistent wage disparities, and longer life expectancies compound this penalty, creating a highly vulnerable financial position for aging women.

Entrepreneurs find it exceptionally difficult to hang up their hats, with 56.4% of self-employed individuals continuing to work while drawing pensions. European and American economic figures show this contrasts sharply with traditional employees, suggesting business owners maintain deeper personal and financial ties to their enterprises well past standard retirement age.

Social Security provides merely a basic foundation, issuing an average monthly benefit of just $2,071 in 2026. This modest stipend barely covers housing and food in many regions, forcing retirees to bridge massive income gaps with private savings or part-time employment.

Outliving savings is now a primary societal phobia, with 48% of workers firmly believing they will outlast their money. This financial fear often surpasses the dread of physical decline, driving many seniors to adopt overly conservative withdrawal rates that paradoxically lower their overall quality of life.

The reality of median balances paints a sobering picture of American wealth; workers aged 65 and older hold a median retirement account balance of just $95,425. Vanguard data demonstrates how heavily top-tier accounts skew average wealth metrics, proving that the typical senior operates with a remarkably thin financial cushion.

Medicare does not cover everything, leaving devastating gaps for long-term care and extended facility stays. Retirees frequently deplete their life savings to qualify for Medicaid when faced with catastrophic cognitive or physical decline, making comprehensive long-term care planning an absolute necessity rather than an optional luxury.

Context and Background

The Great Risk Shift in American Retirement

To understand why modern retirement statistics look so daunting, you must look at the structural changes in how society funds old age. Over the past four decades, the corporate landscape executed a massive transition from defined benefit plans—traditional pensions—to defined contribution plans, primarily the 401(k). When pensions were the norm, your employer bore the market risk and the longevity risk. If the stock market crashed or if you lived to be 105, the company was legally obligated to keep mailing your check. The introduction of the 401(k) fundamentally shifted those risks onto your shoulders. You are now the portfolio manager, the chief risk officer, and the actuary of your own life. This explains why 54% of Americans have zero dedicated retirement savings; the system relies entirely on voluntary participation, high levels of financial literacy, and the disposable income necessary to defer gratification.

The Stealth Tax of Inflation and Longevity

Inflation operates as a silent predator on fixed incomes. When the benchmark for a comfortable retirement jumps from $1.26 million to $1.46 million in a single year, you are witnessing the compounding effect of lost purchasing power. The cost of goods, property taxes, and utility bills establish a new, higher floor that rarely drops back down. When you combine this inflationary pressure with increased life expectancy, the math becomes highly volatile. A generation ago, retiring at 65 meant funding perhaps 10 to 15 years of leisure. Today, medical advancements routinely push lifespans into the late 80s and 90s. Funding a 25-year vacation while the cost of living doubles every two decades requires a massive, growth-oriented portfolio. If your investments are entirely in safe, low-yield bonds, you risk losing your purchasing power over the long haul, directly fueling the fear that nearly half of Americans have regarding outliving their money.

The Complex Web of Senior Healthcare Funding

The $418,000 healthcare price tag for a retiring couple often induces sticker shock because most workers assume Medicare functions as a comprehensive safety net. In reality, Original Medicare requires substantial participation from the patient. Part B, which covers outpatient services and doctor visits, carries monthly premiums that scale upward based on your income. Part D requires you to purchase prescription drug coverage, which fluctuates based on the specific medications you need. Furthermore, Medicare carries deductibles and co-insurance requirements with no absolute out-of-pocket maximum, necessitating the purchase of a Medigap policy. When you aggregate two decades of these premiums, out-of-pocket costs, and specialized treatments not covered by the government—such as dental, vision, and hearing—the expenses easily eclipse a third of a million dollars. Building an aggressively invested Health Savings Account (HSA) during your working years is one of the few tax-advantaged ways you can preemptively attack this looming liability.

Interesting Connections

How Premature Exits Amplify Healthcare Costs

The statistic revealing that 46% of workers retire earlier than planned directly collides with the exorbitant costs of healthcare. When you are forced out of the labor market at age 61 due to corporate downsizing or a personal health crisis, you lose your employer-subsidized health insurance. However, Medicare eligibility does not begin until age 65. This creates a highly dangerous four-year gap where you must secure private health insurance on the open market. Premiums for Americans in their early 60s are incredibly expensive, often eating up massive portions of early retirement withdrawals. This sudden drain forces you to pull heavily from your portfolio during the earliest years of your retirement, exacerbating a financial phenomenon known as sequence of returns risk. A large withdrawal combined with a market downturn early in your retirement can permanently cripple your portfolio’s ability to generate long-term income.

The Link Between Flexible Work and Unretirement

The unretirement trend—where 1 in 8 seniors reenter the workforce—is intricately tied to the modern evolution of the workplace. Historically, returning to work meant enduring brutal commutes and physically demanding labor, which served as a massive barrier for aging adults. Today, the explosion of remote work, gig economy platforms, and flexible consulting roles allows retirees to generate income from their living rooms. While 48% of these individuals return to work out of dire financial necessity, the fact that they can do so is facilitated by digital transformation. You can now leverage decades of industry expertise through project-based contracts, preserving your retirement capital while bridging the gap created by inflation. This remote flexibility transforms retirement from an absolute end date into a gradual tapering of professional responsibilities.

Caregiving Penalties and the Gender Wealth Gap

The 30% retirement savings gap between men and women does not exist in a vacuum; it is the mathematical result of the unpaid caregiving economy. Women are statistically far more likely to leave the workforce or reduce their hours to care for young children, and later in life, to care for aging parents. When you step away from full-time employment during your 30s or 40s, you lose more than just your current salary; you lose employer 401(k) matches, Social Security credits, and the most critical years of compound interest. A dollar saved at age 35 is vastly more powerful than a dollar saved at age 55. Because women also boast longer life expectancies, they must stretch a smaller pool of wealth across a longer time horizon. Mitigating this connection requires aggressive catch-up contributions, spousal IRAs, and ensuring that caregiving households legally and financially share the burden of wealth accumulation.

Frequently Asked Questions

What is the average vs. median retirement savings balance, and why does the difference matter?

When reviewing financial benchmarks, you will often see both average (mean) and median figures, but the median is a far more accurate representation of the typical American’s reality. The average retirement balance is heavily skewed upward by ultra-wealthy individuals holding tens of millions in their accounts. The median balance represents the exact middle point—half of the population has more, and half has less. For Americans over the age of 65, the median balance hovers around $95,000, revealing that the vast majority of retirees are operating with minimal liquid buffers. Relying on average numbers might give you a false sense of societal security, whereas the median highlights the urgent need to build your own robust safety net.

Can I rely entirely on Social Security to fund my retirement?

Relying solely on Social Security guarantees a life of extreme financial constraint. With the average monthly benefit sitting at approximately $2,071, this income stream is designed to act as a poverty-prevention baseline, replacing only about 40% of the average worker’s pre-retirement income. If you live in an area with high property taxes or require ongoing medical care, your Social Security check will likely be exhausted within the first two weeks of the month. You must develop supplemental income streams—through IRAs, 401(k)s, real estate, or taxable brokerage accounts—to ensure you can afford both basic necessities and the lifestyle you envision.

How can I protect my portfolio if I am forced into early retirement?

Since nearly half of all workers leave their jobs sooner than anticipated, you must build emergency flexibility into your long-term plan. The most effective defense is maintaining a robust liquid emergency fund holding one to two years of living expenses in high-yield savings or short-term treasury bills. This cash buffer allows you to survive an unexpected job loss at age 60 without immediately selling off stocks during a potential market downturn. Additionally, keeping your fixed living costs low—such as paying off your mortgage early—drastically reduces the amount of capital you are forced to withdraw when your earned income suddenly stops.

What is the most efficient way to save for healthcare costs in retirement?

The Health Savings Account (HSA) is the single most powerful tool for neutralizing future medical expenses. Available to those with high-deductible health plans, the HSA offers a triple tax advantage: your contributions lower your taxable income today, the investments grow completely tax-free, and your withdrawals remain tax-free as long as they are used for qualified medical expenses. If you pay for current medical bills out of pocket and allow the HSA to compound over two decades, you build a dedicated, tax-free war chest perfectly suited to cover Medicare premiums and out-of-pocket surgical costs in your 70s and 80s.

Why are so many retirees choosing to go back to work?

The resurgence of older adults in the workforce is primarily a response to economic pressure. Persistent inflation erodes the purchasing power of fixed pensions and static bond portfolios, forcing many to seek supplementary income to cover groceries, property taxes, and utilities. However, a secondary factor is the loss of identity and routine. Decades of your life are anchored by the professional challenges and social networks provided by your career. Returning to work, especially in part-time or consulting roles, allows you to alleviate financial stress while reclaiming a sense of purpose and community.