Interesting Connections

Your Social Security benefits function remarkably like an inflation-adjusted single premium immediate annuity, creating a fascinating connection between federal policy and private insurance principles. When you intentionally delay your claim, you essentially purchase additional longevity insurance from the government that powerfully protects you against the devastating risk of outliving your money.

Private insurance companies charge exorbitant upfront premiums for commercial policies offering guaranteed, inflation-linked lifetime payouts, yet the federal government provides this exact financial mechanism simply through delayed retirement credits. You maximize the immense value of this built-in public annuity by leaning heavily on your private investments during your early sixties, allowing your federal benefit to compound untouched until it reaches its maximum possible threshold.

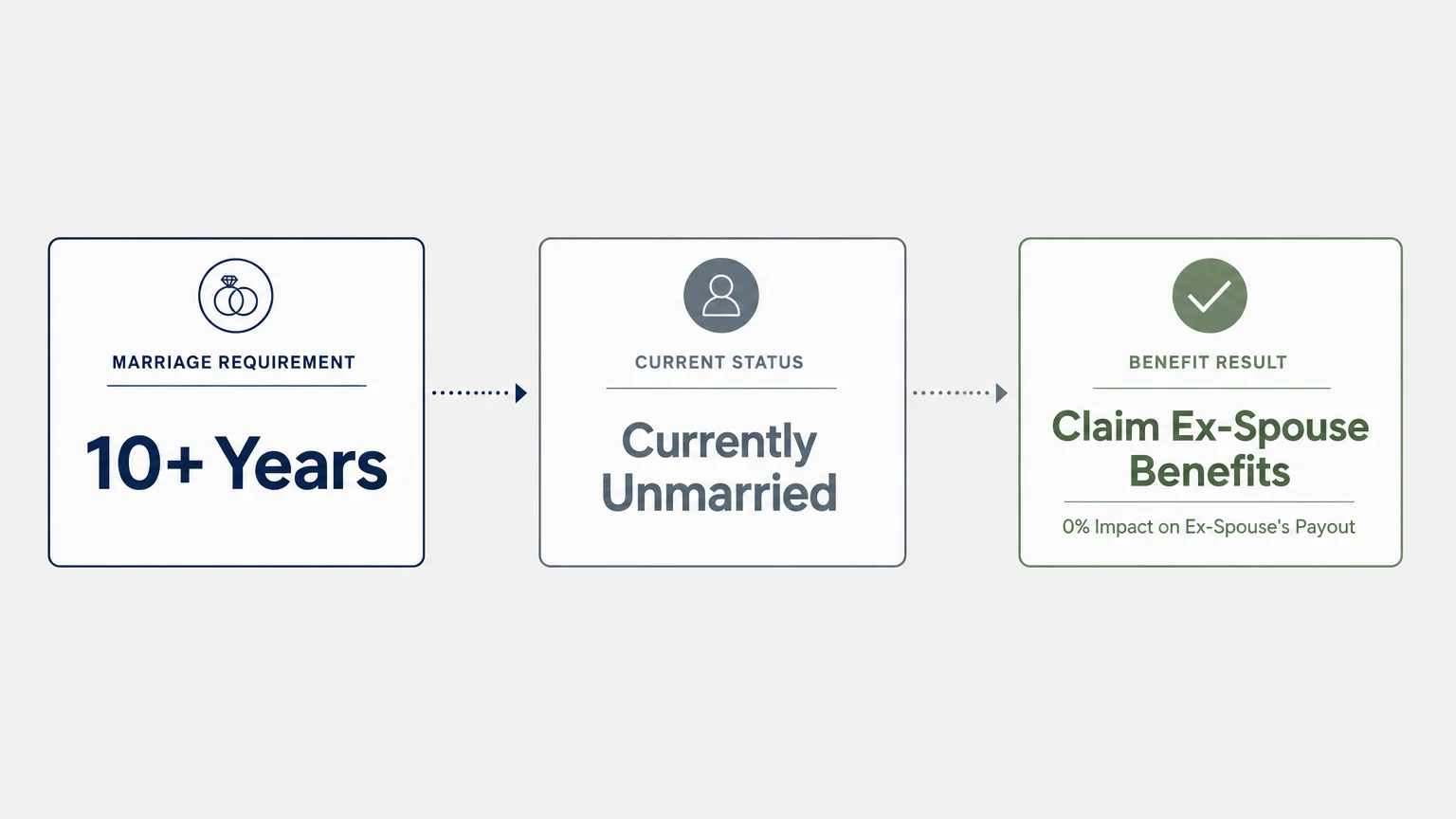

Another compelling intersection exists between your chosen Social Security strategy and your household life insurance needs. Married couples must meticulously coordinate their claiming timelines to protect the surviving spouse, as the death of one partner immediately eliminates the smaller of the two household Social Security checks.

By having the higher-earning spouse aggressively delay their claim until age 70, you definitively guarantee the surviving spouse inherits the largest possible ongoing monthly payment. This strategic delay often radically reduces the necessity for purchasing expensive permanent life insurance policies late in retirement. You can intelligently reallocate the exact money you would have spent on insurance premiums into income-generating assets, effectively utilizing the federal survivor benefit rules to mathematically optimize your broader portfolio.

On a macroeconomic level, the widespread distribution of Social Security funds acts as a crucial, invisible economic stabilizer for local communities across the entire country. Retirees consistently inject their monthly federal checks directly into local grocery stores, healthcare providers, regional retail centers, and local service sectors.

This steady, reliable flow of capital sustains regional economies during severe economic downturns when consumer spending among the working-age population typically contracts. Recognizing this powerful macroeconomic connection highlights exactly why major proposed reductions in federal benefits would trigger widespread secondary effects, damaging local job markets and drastically reducing state and local tax revenues nationwide.

Finally, you must constantly connect your claiming strategy to the broader federal tax code to successfully preserve your retiree finances. Because the IRS strictly calculates your benefit taxation based on your combined provisional income, every single dollar you withdraw from a traditional, tax-deferred retirement account potentially exposes another 85 cents of your Social Security benefit to federal income tax.

You can permanently disrupt this devastating tax torpedo by strategically utilizing Roth accounts throughout your late career and early retirement. Qualified distributions from Roth accounts absolutely do not count toward your provisional income, allowing you to draw substantial tax-free cash while artificially keeping your official IRS income low enough to legally protect your Social Security benefits from excessive taxation. Navigating this complex intersection of tax law and federal benefits defines sophisticated retirement planning.