Fast Facts

Although you pay into the system using after-tax dollars during your working years, the federal government subjects up to 85 percent of your Social Security benefits to income taxes if your combined provisional income exceeds specific IRS thresholds. You must carefully manage your retirement withdrawals from traditional tax-deferred accounts to keep your provisional income low; failure to control these distributions forces you to surrender a massive portion of your earned benefits to excessive federal taxation.

You hold the right to claim benefits based on an ex-spouse’s work record if your marriage lasted at least ten consecutive years and you currently remain unmarried. Accessing this divorced spouse benefit does not reduce the payout your ex-spouse or their current partner receives; it simply leverages their higher earning history to legally boost your personal retiree finances. Taking advantage of this completely independent claiming mechanism secures a larger financial baseline without requiring any communication or coordination with your former partner.

Claiming your monthly check before reaching full retirement age while continuing to work full-time subjects you to the retirement earnings test, which temporarily withholds one dollar in benefits for every two dollars you earn above an established annual limit. Fortunately, the administration does not permanently confiscate this money; they automatically recalculate your benefit formula once you reach full retirement age to slowly return the withheld funds through higher monthly payments over the remainder of your life.

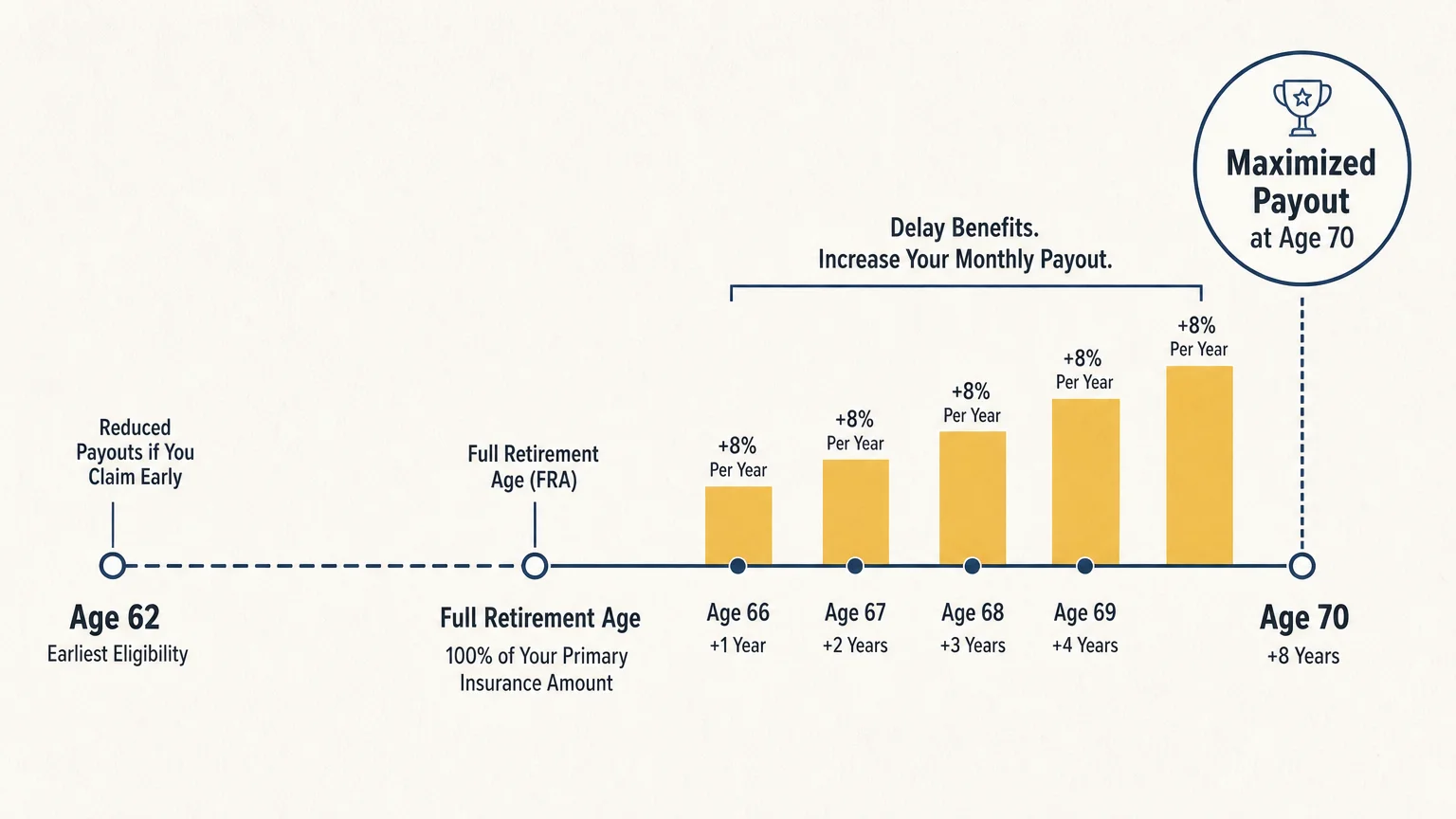

Every single year you delay claiming your benefits beyond your designated full retirement age guarantees an eight percent increase in your monthly payout up until you reach age 70. This delayed retirement credit serves as one of the most powerful tools in retirement planning—offering a guaranteed, inflation-adjusted, risk-free return that absolutely no private market investment portfolio can reliably replicate over a similar timeframe.

Your actual bank deposit often falls surprisingly short of your official benefit amount because the government automatically deducts Medicare Part B premiums directly from your Social Security checks before issuing payment. Furthermore, realizing significant capital gains or executing massive Roth conversions can trigger the Income-Related Monthly Adjustment Amount surcharge; this penalty drastically increases your Medicare premiums and effectively shrinks your net Social Security payout for the entire calendar year.

If you initiate your retirement benefits while actively caring for dependent children under age 18—or under age 19 if they still attend high school on a full-time basis—they individually qualify to receive up to half of your full retirement benefit amount. This family maximum provision provides crucial supplementary income for older parents and grand-families navigating late-stage childrearing, though an overarching cap prevents the combined household payout from exceeding roughly 150 to 180 percent of your foundational base benefit.

Surviving spouses possess the unique, incredibly valuable flexibility to actively coordinate their claiming sequence by drawing a survivor benefit first while allowing their personal retirement benefit to grow untouched, or vice versa. This strategic sequencing requires meticulous calculation but ultimately maximizes your lifetime household payout by ensuring you capture the highest possible delayed retirement credits on whichever earning record yields the largest permanent monthly check.

Annual Cost of Living Adjustments do not merely provide a temporary, isolated inflation hedge; they permanently compound the foundational base figure used to calculate all your future benefit increases. Because these percentage hikes apply directly to your primary insurance amount regardless of your specific claiming age, delaying your application until age 70 mathematically amplifies the absolute dollar value of every subsequent cost of living raise you receive throughout your lifespan.

The poorly understood Windfall Elimination Provision permanently and severely reduces your Social Security payouts if you also collect a pension from a job that did not withhold Social Security payroll taxes, such as specific teaching, police, or state government positions. You must incorporate this aggressive reduction into your retirement planning early, as the regulatory formula can instantly diminish your expected monthly check by more than five hundred dollars and thoroughly shatter your long-term income projections.

Beyond standard federal levies, a minority of specific states currently impose their own localized income taxes on Social Security benefits, utilizing entirely different income thresholds, age brackets, and exemption rules than the federal government. Relocating your primary residence to a tax-friendly jurisdiction can instantly and dramatically improve your retiree finances, though you must comprehensively weigh these specific tax savings against the broader cost of living, healthcare expenses, and property tax rates in your targeted destination state.